If you’re concerned about having enough money in retirement, you’re not alone.

And if you’re behind on savings, you’re in good company there as well. The average American’s 401(k) balance just reached $104,300, while the average IRA balance hit $106,000, according to Fidelity. But while these numbers actually represent an all-time high, they’re not all that substantial in the grand scheme of what most folks need for retirement.

One thing to keep in mind about these figures is that they’re not broken down by age. Rather, they represent averages across all workers, including those who are more advanced in their careers. But even workers in their mid-to-late 30s and 40s should be aiming higher than just over $100,000. If your savings could use a boost, here are a few ways to make that happen in time for retirement.

1. Create a budget

What does following a budget have to do with retirement savings? Everything. Without a budget, you won’t have an accurate means of tracking your spending and identifying ways to save money. And if you can’t manage to save money, you can’t add funds to your IRA or 401(k), thus growing your nest egg.

If you’ve yet to use a budget, here’s some good news: Creating one is easy. Simply list your monthly expenses, factor in sporadic expenses, like that insurance renewal that comes due once a year, and see how much of your income those totals eat up. Then, go through your expenses line by line, figure out which ones will be easiest to cut, and start slashing.

2. Cut corners and bank the difference

If you’re currently spending $500 a month on restaurant meals, that’s a pretty obvious cost to cut. But reducing expenses is much more difficult if you’re already living a relatively frugal lifestyle. Still, you’d be surprised at how much wiggle room you actually have in your budget if you’re willing to make some sacrifices.

For example, you can’t just call up your landlord and tell him you’ll be paying $800 a month for your apartment when your current rent is $1,100. What you can do, however, is move out as soon as your lease expires and find a space that costs $800 a month instead.

Another option? Cut smaller expenses instead of bigger ones, because they will add up. Slashing one restaurant meal per week plus that gym membership you rarely use could easily free up $150 per month, which you can then put into your retirement account. And while that sort of increase may not seem like a lot, consider this: If you save an extra $150 a month for 30 years, and your investments generate an average annual 7% return during that time, you’ll have an additional $170,000 in your retirement plan on top of what you were already saving. Make it $300 a month, and you’ll be looking at $340,000 more.

3. Go heavy on stocks

It’s estimated that 60% of workers invest too conservatively for retirement, and as such, limit their savings’ growth. A better bet? Fill your portfolio with stocks, especially when you’re younger. Doing so will allow you to accumulate wealth more quickly without having to take on unnecessary risk.

Though the stock market is known for its volatility, over time, those who invest in it have a strong tendency to come out ahead. This means that if you have another 30 years in the workforce ahead of you, you can easily put the bulk of your investments into stocks without having to worry each time the market takes a dip along the way.

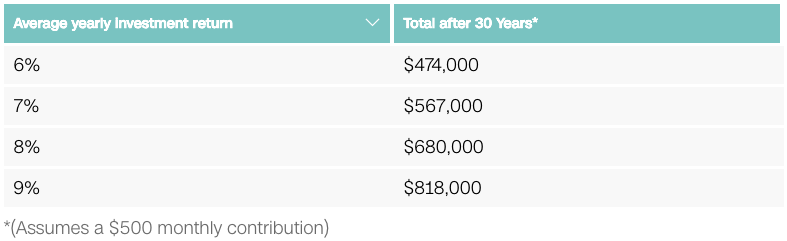

Now check out the following table, which shows how your nest egg might fare over time based on your investments’ performance:

All of these scenarios are plausible with a portfolio that’s mostly stocks with a mix of bonds, but guess which figure most closely mimics the stock market’s average over the past 50 years? That would be the 9% average annual return, and that’s with a major recession thrown into the mix.

Even if you don’t have 30 years of work ahead of you — say you’re already in your late 50s or 60s — you can still feel relatively secure putting most of your money into stocks if you’re not planning to retire for about 10 years. And that’s a great way to buy yourself more financial security as a senior.

Leave a Comment