Today’s investors are spoiled for choice. There are numerous asset classes that you can expose yourself to. And even within just one asset class, there are a ton of choices.

Right now, let’s look at high-quality dividend growth stocks. These stocks represent equity in world-class enterprises that pay reliable, rising dividends to their shareholders. Those reliable, rising dividends are funded by reliable, rising profits.

However, even within just the dividend growth space, there are stocks all over the risk spectrum. Different stocks for different purposes. And today, I want to share with you a low-risk, long-term investment that could be worthy of your capital.

So if you have $1,000 to invest today, and you want to limit your risk, this is definitely an idea for you to consider.

Ready? Let’s dig in.

Timely Dividend Growth Stock to Consider Right Now: Johnson & Johnson (JNJ)

A low-risk, high-quality dividend growth stock potentially worthy of a $1,000 investment right now is Johnson & Johnson (JNJ). Johnson & Johnson is one of my very favorite dividend growth stocks.

This company has quality oozing from every angle. And that’s why its dividend is so reliable. The company has one of the longest and most impressive dividend growth track records in the world.

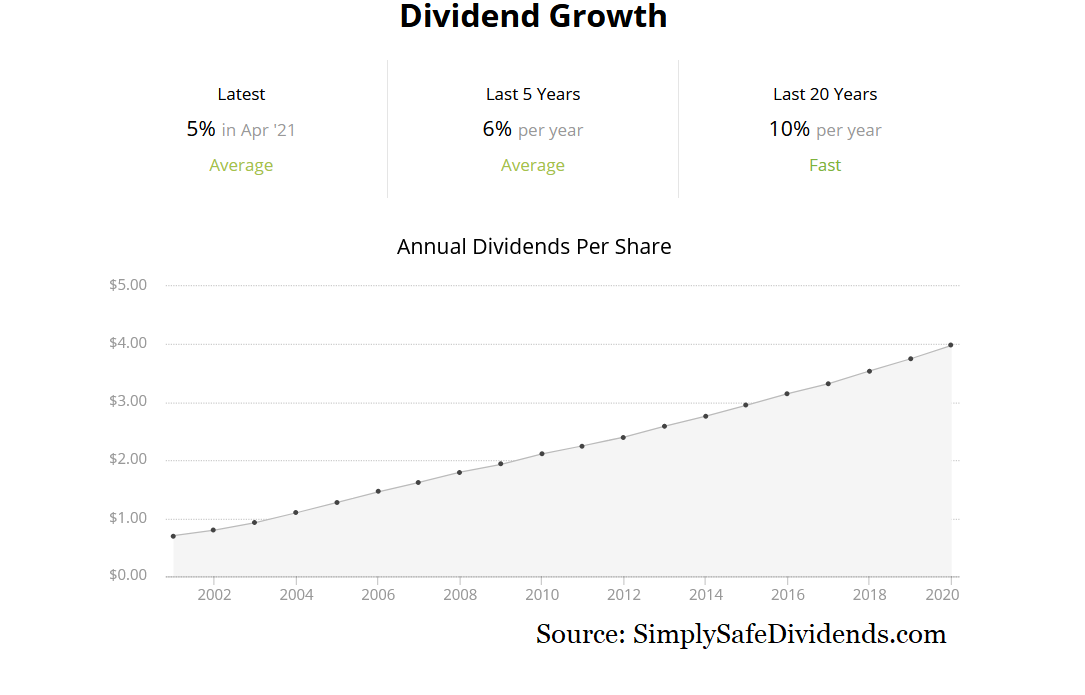

Johnson & Johnson has increased its dividend for 59 consecutive years.

Only the best of the best can do something like that. This Dividend Aristocrat can be the crown jewel of a dividend growth stock portfolio. And with the dividend only costing the company a bit over 50% of free cash flow, the dividend is very safe. Plus, the dividend growth is outpacing inflation – the 10-year dividend growth rate is 6.6%.

Even after almost 60 years into a growth cycle, this dividend is really just getting started in terms of its long-term growth potential.

After all, this company is a healthcare machine. They’re a pharmaceutical business, a medical devices business, and a consumer products business all wrapped up into one company. And with healthcare being a non-discretionary expense with rising demand from a larger world growing older, Johnson & Johnson is positioned about as well as a company possibly could be.

You know what that means? Growing revenue, profits, and dividends.

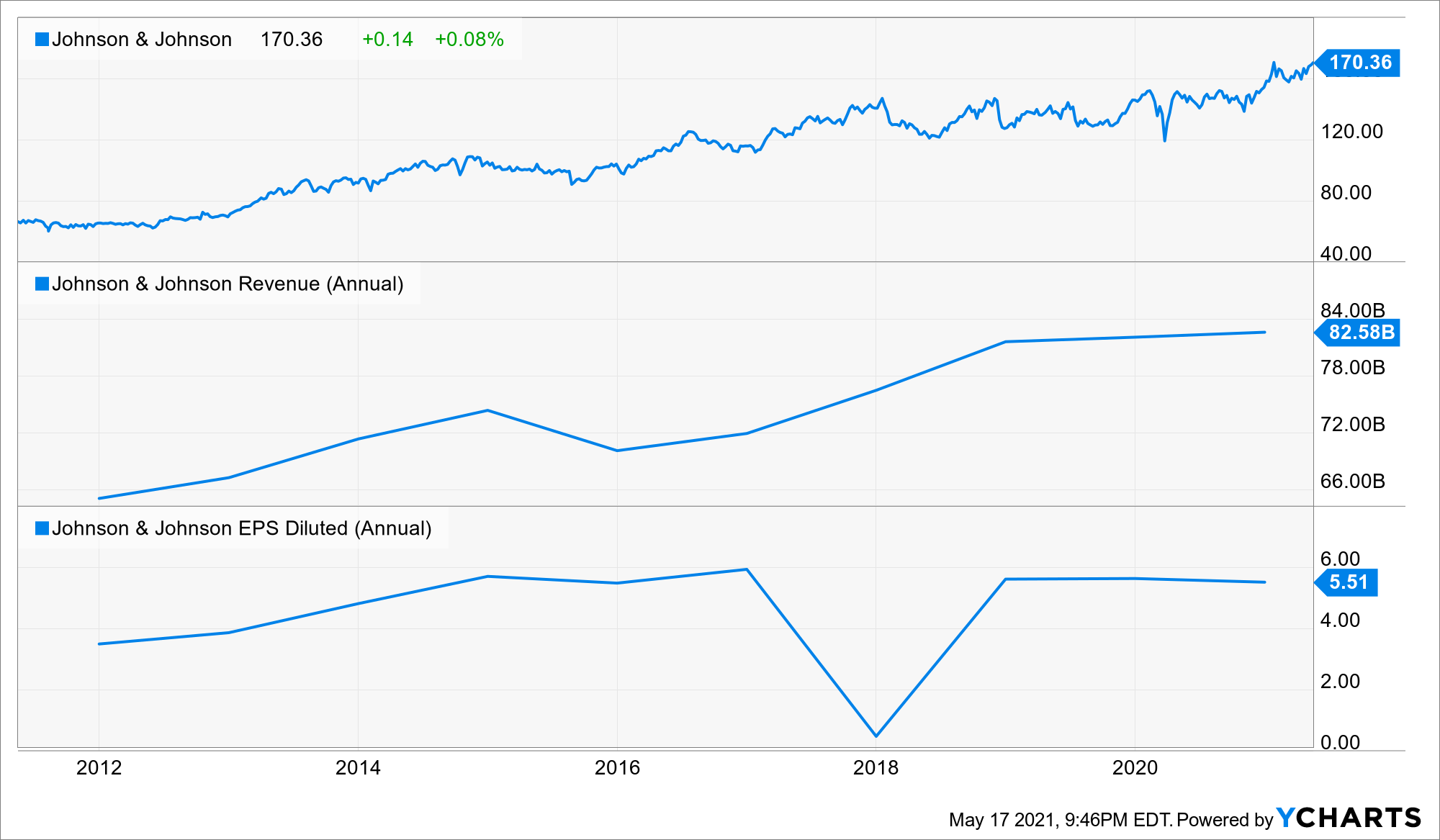

Johnson & Johnson has been able to increase its dividend so consistently because it’s consistently increasing its revenue and earnings. Annual revenue has expanded from $65 billion to more than $82 billion over the last decade. Earnings per share compounded at an annual rate of more than 5% over that period. Now, they’re not going to knock you dead with growth, but this is a low-risk blue-chip business growing at a mid-single-digit rate while you sleep soundly at night.

This stock is also not a bad current income producer – it yields 2.5% here.

No, that’s not a sky-high yield. But again, this is a low-risk play. If you want a 10% yield, you have to assume a ton of risk. Besides, 2.5% smokes the broader market’s yield. And you’re getting inflation-beating growth on top of it. Want more evidence of quality? How about this?

Johnson & Johnson has a AAA credit rating.

They’re one of only two companies in the world that can claim that. Yet even with this blue-chip stock being about as dark blue as it gets, the valuation is reasonable.

The stock trades hands for a forward P/E ratio below 18!

That’s based on the midpoint of guidance for this fiscal year’s adjusted EPS. I do not view that as extreme at all. Not in this market. And not for this level of quality. To be fair, most of the stock’s basic valuation metrics are at or slightly above their recent historical averages. That’s not surprising. The entire market is elevated right now. But I view this as a situation where the stock is simply less of a bargain than it was before instead of a sign of outright expensiveness.

Full story on DividendsAndIncome.com

Leave a Comment